Regulation D Reserve Requirements

Regulation D: Reserve Requirements - A Comprehensive Guide to Understanding the Federal Reserve's Amendments Introduction: The Federal Reserve, commonly referred to as the Fed, plays a crucial role in the United States' financial system. It implements various regulations and policies to ensure the stability and smooth functioning of the economy. One such regulation is Regulation D, which pertains to reserve requirements. In this guide, we will delve into the details of Regulation D and provide a comprehensive understanding of its implications for financial institutions and the economy as a whole. #1. What are Reserve Requirements? The reserve requirements are rules established by the Federal Reserve that determine the minimum amount of funds that banks and other financial institutions must hold in reserve against specific liabilities. These liabilities include transaction deposits, non-personal time deposits, and Eurocurrency liabilities. Reserve requirements are implemented to maintain the stability of the banking system and control inflation. #2. The Purpose of Regulation D: Regulation D, also known as 12 CFR 204, was initially introduced in 1933 as part of the Banking Act. Its primary objective is to establish reserve requirements for depository institutions in the United States. By setting these requirements, the Federal Reserve aims to regulate the lending capacity of banks, control the money supply, and influence short-term interest rates. Reserve requirements serve as a tool for the Federal Reserve to manage the liquidity in the financial system and stabilize the economy during economic fluctuations. These requirements determine the proportion of deposits that banks must hold in reserve, which affects their ability to lend and create a multiplier effect on money supply. #3. Understanding the Recent Amendments: Recently, the Federal Reserve made significant amendments to Regulation D. These changes include adjustments to reserve requirement ratios and the distribution of required reserves. The objectives behind these amendments are to promote stability, enhance the efficiency of the payment system, and maintain appropriate liquidity in the banking system. The amendments to Regulation D also aim to align the reserve requirements with the current financial landscape. As technology evolves and new banking practices emerge, it becomes essential to adapt and ensure that the regulations are effective and relevant. #4. Impact on Financial Institutions: The recent amendments to Regulation D have implications for financial institutions, particularly banks and credit unions. By adjusting the reserve requirement ratios, the Federal Reserve influences the reserves held by depository institutions. The changes in these reserves affect the lending capacity of banks, their profitability, and their ability to meet customer demands. Financial institutions must carefully assess the impact of the amended Regulation D on their operations. They need to evaluate whether they must maintain higher reserves, potentially affecting their ability to make loans and earn interest income. Furthermore, complying with the updated regulations will require financial institutions to review and adjust their internal policies and procedures. #5. Benefits and Challenges of Regulation D: Regulation D, despite its complexities, offers several benefits to the financial system. By establishing reserve requirements, the Federal Reserve ensures that banks have sufficient funds to meet the withdrawal demands of depositors. It enhances the stability of the banking system, reducing the risk of bank runs and ensuring the availability of funds for lending purposes. However, Regulation D also poses challenges for financial institutions. The reserve requirements tie up a significant portion of banks' funds, restricting their lending capacity. This can limit the availability of credit in the economy, making it harder for businesses and individuals to obtain loans. Striking a balance between maintaining adequate reserves and facilitating economic growth is a constant challenge for regulators. #6. The Impact on Borrowers and Consumers: Regulation D and the recent amendments have a direct impact on borrowers and consumers. The reserve requirements affect the availability, cost, and terms of credit. When banks are required to hold higher reserves, they may tighten their lending standards or increase interest rates on loans. This can make borrowing more expensive and potentially reduce the overall credit available to consumers. On the other hand, the stability ensured by Regulation D benefits consumers by maintaining a stable banking system. It provides a level of confidence that their deposits will be safe and accessible when needed. FAQs: Q1: How do the recent amendments to Regulation D affect small banks and credit unions? A: The impact on small banks and credit unions may vary depending on their specific size and financial standing. However, generally, these institutions may face challenges in meeting the new reserve requirements, potentially impacting their lending capacity. Q2: Why does the Federal Reserve adjust reserve requirement ratios? A: The Federal Reserve adjusts reserve requirement ratios to regulate the money supply, control inflation, and manage economic fluctuations effectively. Q3: Do non-depository institutions have to comply with Regulation D? A: No, Regulation D applies to depository institutions such as banks and credit unions that accept deposits from customers. Conclusion: Regulation D and its reserve requirements are vital components of the Federal Reserve's efforts to maintain financial stability. By establishing minimum reserve levels for depository institutions, the Federal Reserve controls the money supply, influences interest rates, and ensures the availability of funds for lending. The recent amendments to Regulation D further enhance the effectiveness of these requirements in the ever-evolving financial landscape. As financial institutions navigate the updated regulations, they must strike a balance between maintaining adequate reserves and facilitating economic growth. Ultimately, a well-regulated banking system benefits both the institutions and the consumers, ensuring stability and accessibility of funds when needed.  Image Source : ifunny.co

Image Source : ifunny.co  Image Source : www.americanbanker.com

Image Source : www.americanbanker.com  Image Source : www.grcsolutions.co

Image Source : www.grcsolutions.co  Image Source : www.lorman.com

Image Source : www.lorman.com  Image Source : edcommstore.com

Image Source : edcommstore.com  Image Source : courses.vubiz.com

Image Source : courses.vubiz.com  Image Source : www.reddit.com

Image Source : www.reddit.com  Image Source : edcommstore.com

Image Source : edcommstore.com

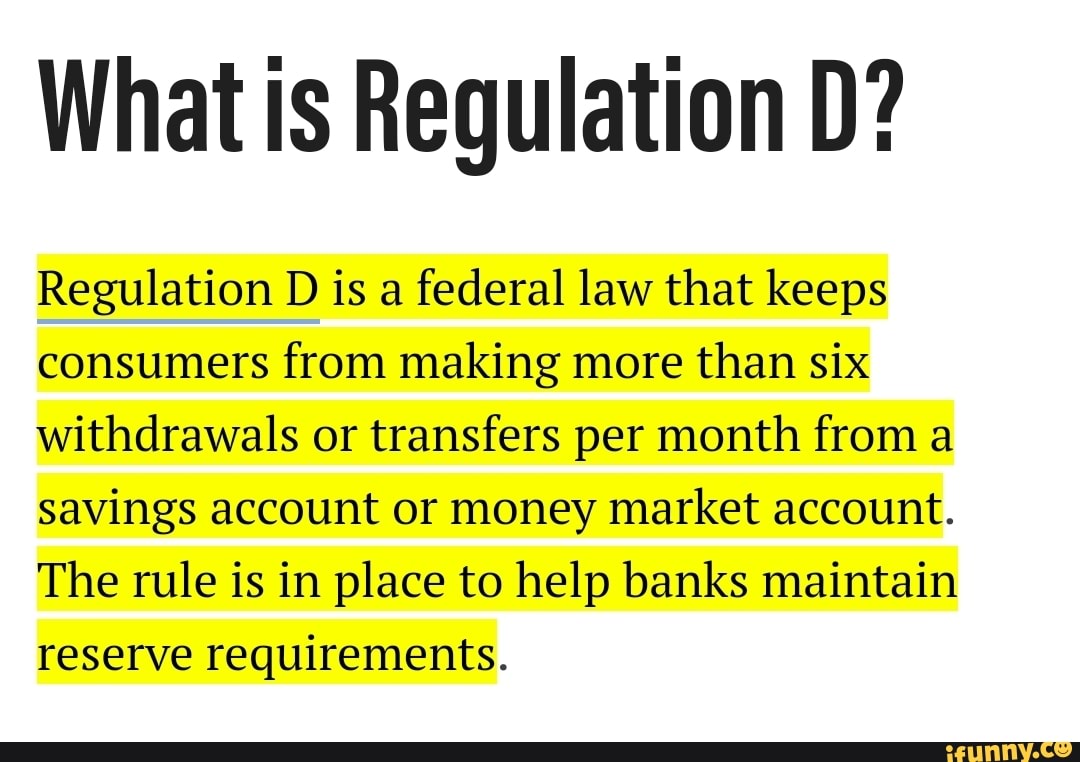

What Is Regulation D? Regulation Federal Law That Keeps Consumers From

Image Source : ifunny.co regulation ifunny federal

Fed Lifts Six-per-month Transaction Limits On Savings Accounts

Image Source : www.americanbanker.com Introduction To Regulation D: Reserve Requirements | GRC Solutions USA

Image Source : www.grcsolutions.co regulation requirements

Regulation D: Reserve Requirements And Compliance - OnDemand Course

Image Source : www.lorman.com Regulation D: Reserve Requirements - Edcomm Group

Image Source : edcommstore.com Regulation D: Reserve Requirements Online Course | Vubiz

Image Source : courses.vubiz.com Aug 26, 2021 - The Federal Reserve Recently Amended Its Regulation D

Image Source : www.reddit.com Regulation D: Reserve Requirements - Edcomm Group

Image Source : edcommstore.com Regulation d: reserve requirements online course. Regulation requirements. Regulation d: reserve requirements. What is regulation d? regulation federal law that keeps consumers from. Regulation d: reserve requirements